Money stress does not usually start in a big, obvious way. It builds slowly.

A few small decisions. A couple of unexpected expenses. A quiet shift in how far your money seems to go. A feeling that things are getting tighter, even if nothing dramatic has happened.

At first, you adjust without thinking too much about it.

You cut back slightly. You delay certain things. You tell yourself you will review everything properly when you have more time, more energy, or when life feels a bit calmer.

But that moment rarely comes. And over time, something begins to change.

You start thinking about money more often than you want to. Not always in a clear or structured way, but in small, repeated thoughts throughout the day.

You feel a slight tension when you need to check your account.

You hesitate before spending, even on normal things.

You replay decisions in your mind after you have already made them.

You might avoid certain conversations altogether.

And slowly, without fully noticing when it happened, money becomes something that sits in the background of your life.

Not loud enough to demand full attention. Not quiet enough to ignore.

Just there.

That is what money stress often looks like in real life.

Not dramatic. Not chaotic. Just constant.

And what makes it harder is that it rarely exists on its own.

It sits alongside everything else you are managing.

Work responsibilities.

Family needs.

Emotional load.

Daily decisions.

Long-term worries.

So even when you try to ignore it, it does not fully leave. If this feels familiar, there is nothing unusual in that.

Many women experience this at different stages of life, especially during seasons where responsibility increases and space for yourself becomes limited.

And one of the most important things to understand is this:

Money stress is not only connected to how much money you have.

It is connected to how things feel.

How clear things feel.

How stable things feel.

How much control you feel you have.

This guide is here to help you reduce money stress in a way that feels manageable and realistic.

Not by trying to fix everything overnight.

But by helping you understand what is happening beneath the surface, and then taking small, steady steps that gradually bring a sense of control back into your finances.

Quick Answer

Reducing money stress does not require fixing everything at once. It comes from understanding your financial situation clearly, simplifying your decisions, and taking small, consistent steps that reduce uncertainty. When you know what is happening and feel able to respond calmly, the pressure begins to ease and you start to feel more in control.

Simple Explanation

Money stress often comes from uncertainty.

Not knowing exactly what is coming in.

Not knowing exactly what is going out.

Not being sure whether what you have will stretch far enough.

Your mind does not settle well with uncertainty. It keeps returning to it, trying to solve it.

Even when you are not actively thinking about money, part of your mind is still holding it in the background, trying to make sense of it, trying to solve it.

That is why money stress is not just practical.

It becomes emotional. It shows up in your thoughts, your decisions, and your daily experience.

You might notice that even when nothing urgent is happening, you still feel slightly on edge.

That is not random. That is your mind responding to a lack of clarity.

This is why small changes can make such a big difference.

Not because they solve everything. But because they reduce uncertainty.

When you move from guessing to knowing, even in a small way, your mind relaxes.

And that shift alone can reduce more pressure than a complicated plan ever could.

A Deeper Look at What Money Stress Feels Like

Money stress is not always easy to recognise because it blends into normal life.

It can feel like:

- A constant low-level tension

- A sense that things are slightly off

- A feeling that you should be doing something, but you are not sure what

It often shows up in subtle ways.

You check your account quickly instead of properly looking.

You delay opening emails related to bills or payments.

You avoid writing things down because it might feel uncomfortable to see everything clearly.

And sometimes, you stay busy. Because staying busy feels easier than sitting down and facing what feels unclear.

None of this means you are bad with money.

It means something does not feel clear or settled. And your mind is responding to that.

Key Takeaways

- Money stress often builds quietly over time, not all at once

- You do not need a perfect system to feel more in control

- Clarity reduces anxiety more than complex budgeting plans

- Small, consistent actions can shift how you feel about money

- Emotional patterns around spending matter just as much as income

- Financial steadiness is built gradually, not instantly

Why Money Stress Happens

Money stress is often reduced to numbers.

Income versus expenses.

Savings versus debt.

But the experience of money stress goes beyond that.

Two people can earn the same amount and feel completely different about their finances.

One may feel steady and in control. The other may feel anxious, uncertain, and overwhelmed.

The difference often comes down to clarity and confidence.

Clarity means you understand what is happening. Confidence means you feel able to respond.

When both are missing, stress increases.

You may find yourself:

- Avoiding your finances altogether

- Feeling anxious before spending

- Overthinking simple decisions

- Feeling guilt even after necessary purchases

- Keeping everything in your head instead of writing it down

These are not just habits. They are signals. Signals that things do not feel clear, safe, or stable.

The Hidden Layer: Mental Load and Money

There is another layer that is often overlooked. Mental load.

For many women, money management does not exist in isolation.

It sits alongside:

- Managing a household

- Supporting children

- Planning meals

- Tracking appointments

- Remembering responsibilities

So money decisions are not just financial. They are part of a much larger mental system.

And when that system is already full, even small financial decisions can feel overwhelming.

It is not because they are complicated. It is because there is very little space left to process them well.

This is why simplifying your finances matters so much.

Not because simple sounds nice. Because it gives your mind less to carry.

Common Causes of Financial Pressure

Money stress usually does not come from one single issue. It is often a combination of factors that build up over time.

Rising living costs

Even small increases create pressure over time. It is not always a sudden jump. It is gradual.

Food becomes slightly more expensive.

Bills increase slightly.

Everyday spending edges up.

And without noticing, your margin reduces. That reduction creates tension.

Lack of clarity

This is one of the biggest drivers of stress.

When you do not fully know what is happening, your mind fills in the gaps.

And it rarely fills them with calm or neutral thoughts. It often assumes the worst. Clarity removes that.

Irregular or stretched income

Even when income is steady, if it feels stretched, it can create the same effect as irregular income.

You may feel like you are constantly trying to make things fit. That feeling creates pressure.

Emotional spending

Spending is not always logical.

Sometimes it is tied to:

- Feeling tired

- Feeling overwhelmed

- Wanting a break

- Wanting something that feels like relief

And in the moment, it can feel justified. But repeated over time, it can quietly increase financial pressure.

Life transitions

This is where money stress often deepens.

Changes in life bring both emotional and financial shifts.

Career changes

Parenting demands

Health considerations

Supporting others

These moments require adjustment. And adjustment takes energy.

Why This All Feels So Heavy

Money touches areas of life that feel important.

Security

Stability

Responsibility

Freedom Choice

So when something feels uncertain, it rarely stays small. It expands. And it shows up in everyday life.

You might be trying to relax, but your mind returns to money. You might be making a simple decision, but it feels heavier than it should.

This is not because you are overreacting. It is because your mind is trying to resolve something that feels unclear.

A Small but Important Shift

Instead of asking: How do I fix everything?

Shift to: What can I make clearer today?

That question changes everything. Because clarity is the starting point of control.

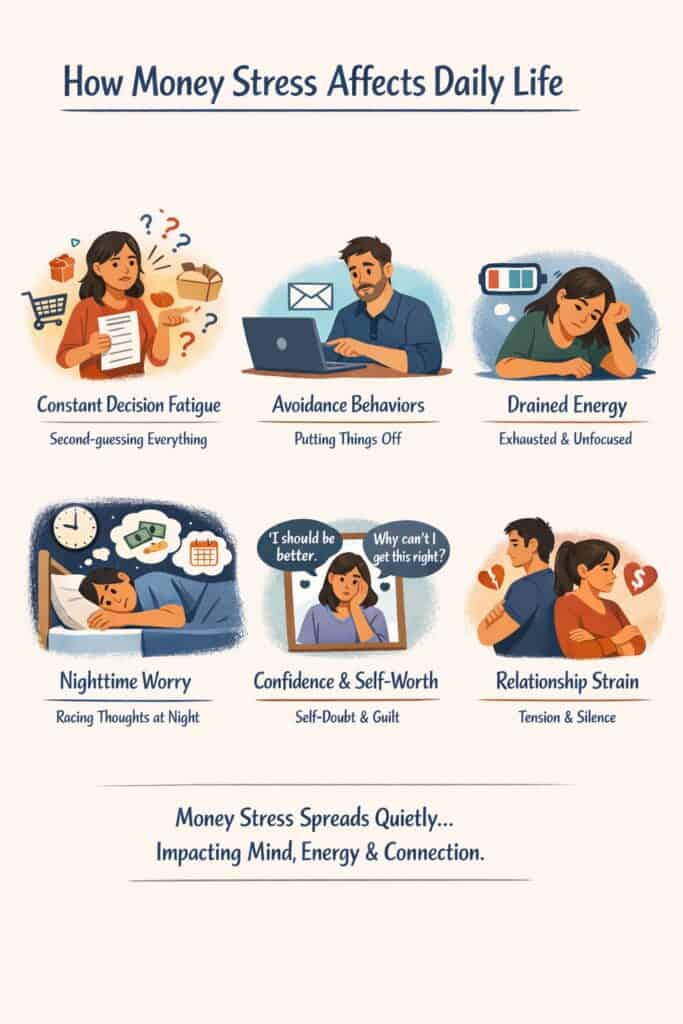

How Money Stress Affects Daily Life

Money stress does not stay in one place.

It spreads quietly into how you think, how you decide, and how you move through your day.

Decision fatigue becomes constant

When money feels uncertain, every decision starts to carry weight.

Even simple things like:

- What to buy at the shop

- Whether to order food or cook

- Whether to say yes to something

You may notice hesitation where there used to be ease.

It is not because the decision is big. But because your mind is already holding so much.

You start second-guessing yourself

You might make a decision, then revisit it later.

Should I have done that

Did I need that

Was that the right choice

This repeated questioning slowly reduces your confidence.

Not just with money. But in general.

Avoidance becomes a coping strategy

Avoidance often looks like:

- Not checking your account properly

- Ignoring certain emails

- Putting off decisions

It feels like relief in the moment.

But underneath, the pressure builds. Because what is unclear does not disappear.

Your energy gets affected

Money stress is not just mental. It drains energy.

You may feel:

- More tired than usual

- Less focused

- Less motivated to deal with things

Because part of your mind is always working in the background.

It can affect sleep

Money stress often follows people into the evening.

That is when the day quiets down and the thoughts become louder.

What is due next week

Whether there is enough

What you forgot

What needs sorting

Even if you are tired, your mind may not switch off easily.

It can affect confidence and self-worth

This part matters. Money stress can easily turn into personal judgement.

You may start telling yourself stories like:

- I should be better at this

- I should have sorted this sooner

- Why does this feel so hard

- Other people seem to manage better

But money stress is not proof that you are failing.

It is often a sign that too much feels unclear, stretched, or emotionally loaded.

It quietly affects relationships

Money can create tension even when it is not openly discussed.

Different expectations

Different comfort levels with spending

Unspoken concerns

Even silence can carry pressure.

Emotional Spending and Why It Happens

Emotional spending is often misunderstood.

It is not just “bad habits” or lack of discipline.

It is usually a response. A response to how you are feeling.

What emotional spending is really doing

In many cases, spending is meeting a need.

Not a financial need. A human one.

You might be seeking:

- Relief after a long day

- Comfort when things feel heavy

- A sense of control when life feels uncertain

- A small moment that feels like it belongs to you

- A reward after carrying too much for too long

And in that moment, spending works. It gives a quick shift.

It changes how you feel for a little while. That is why it can become hard to break.

Why it becomes a pattern

The problem is not the moment itself. It is the repetition.

When spending becomes the default way to create relief, it starts to build pressure instead of reducing it.

And then a cycle forms:

Stress ? spending ? temporary relief ? guilt ? more stress

That cycle can be quiet.

It does not always show up as dramatic overspending.

Sometimes it looks like small repeated purchases that do not feel huge in the moment but add up over time.

The emotional side of convenience spending

Not all emotional spending looks obvious.

Sometimes it looks like paying for convenience because you are exhausted.

Takeaway because you cannot face cooking.

Buying something quickly because you do not have the energy to compare options.

Letting subscriptions continue because cancelling them feels like another task.

This does not make you irresponsible.

It means energy matters. Capacity matters.

And money decisions are often shaped by how tired you are.

A calmer way to approach it

The goal is not to eliminate emotional spending completely.

That creates more pressure. Instead, begin to notice it.

Ask: What did I need in that moment?

Was it rest

Was it comfort

Was it a break Was it relief

Was it something that felt like care

Once you understand the need, you can start creating alternatives.

Not perfect ones. Just slightly better ones.

A break that does not involve spending.

A comfort routine that costs little or nothing.

A pause before checkout.

A habit of waiting until the next morning.

If you want to understand your own patterns more clearly, you can explore this reflection tool: Emotional Spending Awareness Quiz,

Small Changes That Actually Reduce Money Anxiety

This is where things begin to shift in a real way.

It is not through big changes. But through small, steady ones.

1. Sit with your numbers without pressure

Not to fix anything. Just to see. This alone can feel uncomfortable at first.

But it removes guessing. And guessing is what fuels anxiety.

You do not need a perfect spreadsheet. A notebook page is enough.

A simple note on your phone is enough. What matters is seeing what is there.

2. Take things out of your head

When everything stays in your mind, it feels bigger than it is.

Write things down:

- Income

- Bills

- Spending

- Upcoming payments

- Things you are worried you might forget

Clarity reduces mental load immediately.

If you want help spotting patterns, use this Spending Habits Clarity Quiz.

3. Reduce the number of decisions you make

Too many choices create overwhelm. Simplify where you can.

For example:

- Have a general weekly spending amount

- Decide certain things in advance

- Choose a regular food shop budget

- Keep a short list of default meals

- Set simple rules for non-essential spending

This removes constant decision-making.

4. Focus on one area only

Trying to fix everything creates pressure.

Choose one:

- Food spending

- Subscriptions

- Daily spending

- Online shopping

- Impulse purchases

Start there. A smaller focus makes progress feel possible.

5. Keep your money visible

Avoidance increases stress. Visibility reduces it.

That does not mean staring at your account all day. It means not hiding from it.

A short weekly check-in often helps more than constant anxious checking.

6. Build one calming habit

One calming money habit is better than five complicated ones you cannot maintain.

A weekly review.

A no-buy day.

A pause before checkout.

A Sunday reset.

Pick one and stay with it.

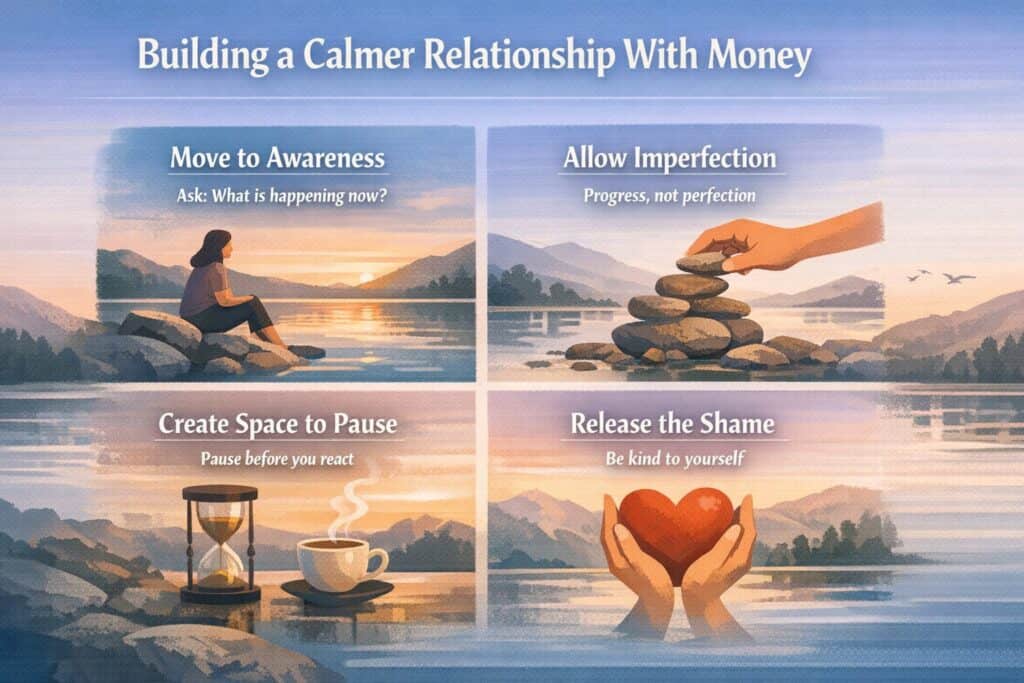

Building a Calmer Relationship With Money

This is where deeper change happens.

Because how you feel about money shapes how you behave with it.

If money feels tense, every decision carries tension. But this can shift.

1. Move from pressure to awareness

Instead of asking: What do I need to fix?

Ask: What is happening right now?

Awareness creates space. It slows the panic. It makes decisions clearer.

2. Allow things to be imperfect

Waiting for everything to be perfect delays progress.

You can work with what is real now. Even if it is not ideal.

Even if there are things you wish were different.

Even if you feel behind. Progress does not require perfect conditions.

3. Create space before reacting

When you pause, even briefly, you move from reaction to choice.

That shift matters more than you think.

A few minutes.

A few hours.

One night of waiting.

Those small pauses reduce emotional decisions and increase calm ones.

4. Stop using shame as a motivator

Shame does not create steadiness. It creates avoidance.

If your inner voice gets harsh every time money feels difficult, the whole process becomes heavier.

A steadier voice helps more.

One that says:

- This feels difficult right now.

- Let me look clearly.

- Let me take the next step.

That tone creates movement.

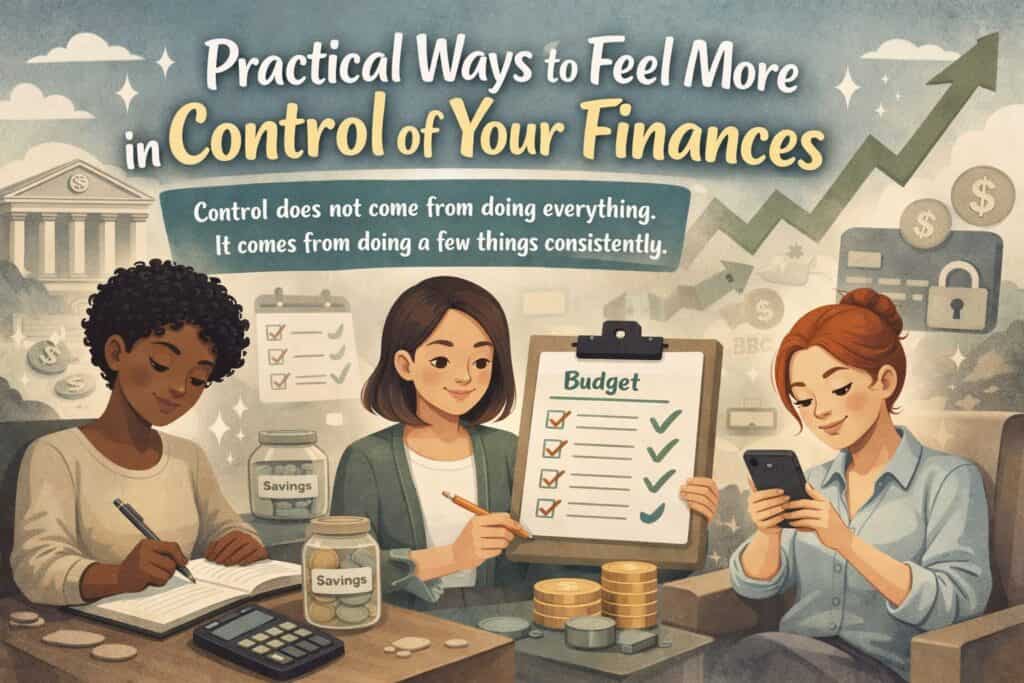

Practical Ways to Feel More in Control of Your Finances

Control does not come from doing everything. It comes from doing a few things consistently.

1. Create a weekly money check-in

This is one of the most powerful habits you can build.

Set aside 15–20 minutes once a week.

Not to fix everything. Just to stay connected.

During that time:

- Check your balance

- Look at recent spending

- Note anything upcoming

- Review one area you want to understand better

That is enough. Consistency matters more than detail.

2. Reduce financial decision fatigue

Decide some things in advance.

For example:

- A weekly spending range

- What you prioritise

- What you are not focusing on right now

- What counts as a pause-before-buying purchase

This reduces daily mental effort.

3. Use simple rules

Instead of complex systems, use small rules.

Pause before non-essential spending.

Wait 24 hours if unsure.

Choose calm over urgency. Do not buy late at night when tired

Review subscriptions once a month

Simple rules reduce emotional decisions.

4. Keep money visible

Even a simple list is enough.

Income.

Bills.

Essentials.

Flexible spending.

Next priorities.

It does not need to look impressive. It needs to be usable.

Use check-ins when you feel emotionally flooded

Sometimes money stress and emotional overwhelm rise together.

That is when it helps to slow down before making decisions.

These Self-Care Check-Ins – Simple Reflection Tools may help.

Calm Budgeting (Without Pressure or Overwhelm)

Budgeting is where many people start to feel stuck. Not because they do not want to manage their money.

But because the way budgeting is usually presented feels rigid, overwhelming, and unrealistic for real life.

Spreadsheets.

Dozens of categories.

Tracking every transaction.

Trying to get everything exactly right.

That level of detail can work for some people. But for many, it creates pressure.

And when something feels heavy, it becomes something you avoid.

Calm budgeting removes that pressure. It gives you structure without making you feel restricted.

It helps you stay aware of your money without needing to control every detail.

And most importantly, it is something you can keep going with.

What Calm Budgeting Looks Like in Real Life

Calm budgeting is simple. Not basic. Not careless.

Just simple enough to be sustainable. You are not tracking every dime.

You are not aiming for perfection.

You are creating a clear view of what is happening, so your decisions feel easier.

That is what makes the difference.

When something feels manageable, you come back to it. And that is where real change happens.

A simple structure that works

Instead of building a complicated system, start with three categories:

- Essentials

- Flexible spending

- Future

That is enough.

You do not need ten categories. You do not need detailed breakdowns.

Too much detail creates friction. And friction leads to avoidance.

Keeping it simple keeps you consistent.

Understanding Each Category Properly

Essentials

These are the costs that keep your life running.

Rent or mortgage

Utilities

Food

Transport

Insurance

Basic household expenses Minimum debt payments if relevant

These are necessary.

But even here, awareness matters. Not to cut everything down. But to understand what is happening.

Many people carry stress here simply because they have not looked closely in a while.

Clarity removes that layer of uncertainty.

Flexible Spending

This is where most money stress builds.

Not because spending here is wrong. But because it is often unstructured.

This includes:

- Eating out

- Shopping

- Subscriptions

- Convenience spending

- Lifestyle choices

When this area is unclear, your mind keeps returning to it.

That is where second-guessing comes from. That is where guilt comes from.

Giving this category a loose structure reduces that pressure. Not strict rules.

Just awareness and a general limit.

Future

This is not only savings. This is stability.

It includes:

- Savings

- Emergency buffer

- Debt repayment if needed

- Anything that supports your future self

Even a small amount here changes how things feel. Because it introduces a sense of safety.

And that sense of safety reduces stress in a way that income alone does not.

How to apply it in real life

Start with what you already have.

Look at your income. Then divide it roughly into the three categories.

Not perfectly. Just honestly.

What is going to essentials

What is going to flexible spending

What is going toward future stability

That simple view can bring immediate relief.

Because you are no longer trying to carry it all in your head.

Why this approach reduces stress

Because it removes complexity. You are not constantly calculating.

You are not turning every spending choice into a full emotional event.

You have a general sense of direction. And that creates calm.

What calm budgeting is not

It is not punishment.

It is not a system built on guilt.

It is not cutting out every small pleasure.

It is not pretending that life is neat and predictable.

A calm budget leaves room for real life.

It helps you stay connected to your money without making money the centre of every thought.

Building Financial Steadiness

Steadiness is not about having more money. It is about feeling grounded.

You can earn more and still feel stressed all the time.

You can earn less and feel more settled because your money is clearer, simpler, and more intentional.

Financial steadiness grows through small repeated actions.

Step 1: Visibility

Know what is happening. Even roughly.

You do not need perfect numbers to begin. You need honesty.

What is coming in

What is going out

What is due soon

What feels unclear

That is enough to start.

Step 2: Reduce uncertainty

Choose one unclear area and make it clearer.

It might be:

- Upcoming bills

- Your true monthly essentials

- Subscriptions

- Food spending

- Debt payments

- How much is disappearing on small purchases

You do not need to clear every unknown at once. One area is enough.

Step 3: Create breathing room

Even a small buffer helps.

It changes how things feel. It reduces urgency. It gives you a little more space to respond instead of panic.

This does not have to start big.

A small emergency cushion.

A sinking fund for a regular cost.

A little money set aside for the unexpected.

Breathing room builds steadiness.

Step 4: Repeat simple habits

Consistency creates stability.

Not intensity. Not one dramatic reset. Not one perfect month.

Simple repeated habits build financial steadiness far more effectively than extreme effort you cannot sustain.

Step 5: Make your system easier to return to

This matters. The best money system is not the most detailed one.

It is the one you can return to when life gets busy.

That means:

- Simple categories

- Short check-ins

- Clear priorities

- Low friction

A system that is easy to restart is a strong system.

Money Stress Triggers You May Not Notice

Sometimes money stress does not come from one obvious financial problem.

Sometimes it comes from patterns that seem small on their own, but heavy when they build up.

This matters because many people assume they would only feel stressed if something dramatic had gone wrong.

But money stress can build quietly through repeated friction.

A few examples:

- You keep spending small amounts without really noticing

- You feel pressure to say yes to things you cannot comfortably afford

- You are too tired to plan, so convenience spending increases

- You have subscriptions or recurring costs you have not reviewed in months

- You compare yourself to people whose full financial reality you do not know

- You keep telling yourself you will sort things out later

- You avoid checking certain numbers because they make you feel tense

None of these automatically mean you are in crisis. But they do create mental drag.

And mental drag is one of the reasons money stress feels so constant.

It is not always the size of the problem.

Sometimes it is the repetition. Sometimes it is the feeling that money keeps leaking energy from you in small ways all week long.

If money has been feeling heavy but hard to explain, pause and reflect before trying to fix everything at once.

You can explore the free tools here.

Start with one. That is enough.

Small Ways to Regain Control When Money Feels Messy

One of the hardest parts of money stress is that it can make everything feel bigger than it is.

Not always because the situation is simple. But because your mind is trying to carry too much at once.

When that happens, the goal is not to solve your whole financial life in a day.

The goal is to regain some ground.

A little clarity.

A little steadiness.

A little breathing space.

That matters more than people think.

Start with what is true now

A lot of people delay looking at their money because they want to feel ready first.

But readiness often comes after the first step, not before it. So begin with what is true now.

What is in your account.

What is due soon.

What feels unclear.

What you have been avoiding.

Do not start with what you wish were true. Do not start with an ideal version of your finances.

Start with what is real. That is where steadiness begins.

Shrink the size of the task

Money stress gets heavier when everything feels like one giant problem.

Break it down.

Do I need to understand my bills better?

Do I need to look at my food spending?

Do I need to stop avoiding my balance?

Do I need to review my subscriptions?

A smaller question is easier to answer. And smaller answers build momentum.

Choose one pressure point

If you try to tackle everything at once, you will probably end up feeling flooded again.

Choose one area that feels heaviest right now.

It might be:

- Unexpected spending

- Food costs

- Impulse buying

- Debt anxiety

- A lack of savings

- General avoidance

Pick one and give it proper attention. You are far more likely to make progress that way.

Replace vague worry with a simple note

Vague worry keeps circling. A written note grounds it.

Try this:

- What feels stressful right now?

- What do I know for sure?

- What am I assuming?

- What is the next useful step?

That kind of simple written check-in turns mental noise into something you can work with.

Use a short weekly reset

A weekly money reset does not need to be long. Ten to twenty minutes can be enough.

Look at what came in.

Look at what went out.

Check what is coming up.

Note anything you need to adjust.

That one habit can stop money stress from building in silence.

Let your system be imperfect

This matters more than many budgeting articles admit.

A system that is slightly messy but used regularly is more helpful than a perfect system you avoid.

A short list you actually look at beats a beautiful spreadsheet you never open.

A simple note on your phone beats an advanced budget app that makes you feel behind.

Use what works. Not what looks impressive.

Final Thoughts

Money stress does not arrive all at once. And it does not disappear all at once either.

It builds gradually.

Through small moments.

Through repeated patterns.

Through things left unclear.

And because of that, it softens in the same way.

Through small steps.

Through clearer understanding.

Through decisions that feel manageable.

You do not need to solve everything. You do not need to get everything right.

You just need to feel a little more steady than you did before. And that is something you can build.

Slowly.

Calmly.

In a way that actually lasts.

Frequently Asked Questions

Why does money stress affect mental health?

Money is linked to security and stability. When it feels uncertain, your mind stays alert and keeps returning to it. Over time, this can lead to anxiety, tension, and difficulty relaxing.

How can I stop worrying about money constantly?

Start by creating small moments of clarity. When you understand your finances better, your mind has less uncertainty to focus on. Even simple awareness can reduce constant worry.

What are the signs of financial stress?

Common signs include avoiding your finances, feeling anxious about spending, overthinking decisions, difficulty sleeping, and a constant sense of worry about money.

How can I feel more in control of my finances?

Focus on small, consistent actions. Know your numbers, simplify decisions, and create a basic structure that feels manageable.

Does budgeting really help with money stress?

Yes, but only if it feels simple and realistic. Overly complex budgets can increase stress. Calm, flexible budgeting is more effective.

What is emotional spending?

Emotional spending happens when money is used to cope with feelings such as stress, boredom, or overwhelm. Understanding the reason behind it is the first step to changing it.

How long does it take to reduce money stress?

It takes time. Money stress usually builds gradually, and it reduces in the same way. Small changes, repeated over time, create steadiness.

Can I feel financially stable without earning more money?

In many cases, yes. Stability often comes from clarity, structure, and confidence in managing what you already have.

If this helped you think about money differently

Share it with someone who needs less stress and more clarity.

Pin it, send it, or save it for later.

And if you want more calm, practical guidance around financial self-care, subscribe and receive a free guide:

The Calm Life Reset Guide – 10 small shifts that reduce overwhelm and money stress.